The Goods and Services Tax (GST) is one of the biggest tax reforms in India, introduced to create a unified tax system across the country. Since its launch on July 1, 2017, GST has revamped the Indian tax structure by merging several indirect taxes into a single umbrella.

It streamlined taxation, improved compliance, and helped create a transparent system. Let us look at the Top 31 best objectives of GST in this blog post and how it seeks to transform the Indian economy.

What is the Goods and Services Tax?

A unified, destination-based, and multi-stage tax on goods and services, GST subsumes all the various indirect taxes existing in India, except a few; it replaces them all with a single tax to achieve a better system of taxation.

If you want to know more about the goods and services tax then just click on the below video:

What are the Top 31 Objectives of GST?

We have told you all about the top 31 objectives of GST, for understanding, all their names are written below, after which the main information about all of them will also be given below:

- Eliminate the Cascading Effect of Taxes

- Create a Unified National Market

- Simplify Tax Structure

- Boost Government Revenue

- Promote Competitive Pricing

- Enhance Ease of Doing Business

- Encourage Exports

- Promote Digital Compliance

- Curb Tax Evasion

- Increase Taxpayer Compliance

- Achieve Economic Efficiency

- Reduce Informal Economy

- Enhance Competitiveness in Domestic and International Markets

- Foster Cooperative Federalism

- Online Procedure

- Remove Multiple Indirect Taxes

- Increasingly Efficient Logistics

- Review Tax Revenue

- Uplifting GDP

- Better Tax Management

- Broadening the Tax Base

- Composition Scheme for Small Businesses

- Regulation of Unorganized Sector

- To Increase the Productivity

- To Reduce the Prices

- Dynamic Common Market

- Simplification of Taxation

- Streamlined Online Procedures

- A Uniform Tax System

- Enhanced Productivity of Logistics

- GST Rates on Goods and Services

Eliminate the Cascading Effect of Taxes

GST eliminates the phenomenon of cascading effect or “tax on tax”. In the pre-GST era, businesses had to pay tax not only on inputs but also on the final product. Thus, the overall tax burden increased significantly.

GST achieves taxation only on the value added at each stage of production or service, thus reducing the overall liability and making goods cheaper.

Elimination of cascading effect of taxes in GST is the 1st objective among objectives of GST and also a very important one.

Create a Unified National Market

GST has integrated India as a common market as the tax barriers that separated the states have now been removed. Thus, the free movement of goods and services across the borders of a state has brought down logistics costs to its minimum while boosting trade. A single tax regime will allow businesses to operate as a single market across India.

Create a Unified National Market is the 2nd objective among objectives of GST and also a very important one.

Simplify Tax Structure

Before GST, businesses had to deal with multiple taxes including VAT, excise duty, and service tax, each of which had different compliance rules, making the process complex and less understandable.

Simplify Tax Structure is the 3rd objective among objectives of GST and also a very important one.

Boost Government Revenue

The GST system has broadened the tax base and improved compliance. Since the transactions are digital and the nature of the tax system is also digital, it helps the government to prevent tax evasion and ensure a steady flow of revenue.

Boost Government Revenue is the 4th objective among objectives of GST and also a very important one.

Promote Competitive Pricing

This has reduced the overall tax burden for manufacturers and suppliers. This has led to savings which manufacturers and suppliers will be able to pass on to consumers in the form of lower prices. This has been useful in promoting healthy competition for businesses in terms of cost reduction and price improvement for end users.

Promote Competitive Pricing is the 5th objective among objectives of GST and also a very important one.

Enhance Ease of Doing Business

The GST system with uniform tax rates and online compliance mechanisms has eased the operational process for businesses. Thus, by eliminating multiple taxes and reducing compliance requirements, India has improved its ranking in the global index of ease of doing business.

Enhance Ease of Doing Business is the 6th objective among objectives of GST and also a very important one.

Encourage Exports

Another area where GST has played a vital role recently is in promoting exports. Tax neutrality on goods and services for international markets has boosted exports. Indian goods can now be made more competitive in the global market by making them cost-effective by providing an option to claim refunds on input taxes.

Encourage Exports is the 7th objective among the objectives of GST and also a very important one.

Promote Digital Compliance

GST will promote and facilitate a 100% digital process for tax returns, payments, as well as refunding. Key online systems like e-way bills and e-invoicing would be of immense help in compliance with the tax norms by businesses while the government gets to realize real-time monitoring with lots of transparency.

Promote Digital Compliance is the 8th objective among the objectives of GST and also a very important one.

Curb Tax Evasion

This ITC under GST can ascertain input tax credit only when suppliers have paid their GST. Thus, through the chain of liability, the chances of evasion are reduced and the tax collected is subsequently enhanced.

Curb Tax Evasion is the 9th objective among the objectives of GST and also a very important one.

Increase Taxpayer Compliance

Under GST, online and automated procedures make tax compliance easy for the business. Standardized forms, few taxes to deal with, and transparent procedures lead to a higher rate of compliance with taxes where businesses face no issues in meeting their taxes.

Increase Taxpayer Compliance is the 10th objective among the objectives of GST and also a very important one.

Achieve Economic Efficiency

This increases economic efficiency because taxes on goods and services are reduced. All multiple taxes are eliminated, and there is a single system that makes production faster, allocates resources more accurately, and makes the entire economy more efficient.

Achieve Economic Efficiency is the 11th objective among the objectives of GST and also a very important one.

Reduce Informal Economy

GST has encouraged businesses to move into the formal economy. Input tax credits and easier compliance regimes have meant that more companies have chosen to register under GST than would have otherwise. This has reduced the size of the informal sector and contributed to formal tax revenues.

Reduce Informal Economy is the 12th objective among the objectives of GST and also a very important one.

Enhance Competitiveness in Domestic and International Markets

GST can actually help Indian goods and services become more competitive by reducing the overall cost of production and ensuring that tax is levied only on added value. Exports increase, and India becomes a meaningful and competitive player in global trade.

Enhance Competitiveness in Domestic and International Markets is the 13th objective among the objectives of GST and also a very important one.

Foster Cooperative Federalism

Such a federal taxation structure implements GST, which combines the interests of the central and state governments. The policy and rate decisions of such taxation are made within the GST Council, which has members from both levels and is therefore created collaboratively, making it a symbol of cooperative federalism and a smooth implementation process across the country.

Foster Cooperative Federalism is the 14th objective among the objectives of GST and also a very important one.

Online Procedure

Under GST, the entire process – from registration to payments and returns – will be online, reducing paperwork, speeding up processes, and leading to efficient business operations, as well as more effective government tracking.

Online Procedure is the 15th objective among the objectives of GST and also a very important one.

Remove Multiple Indirect Taxes

GST has replaced the tax system under which there were a plethora of indirect taxes at both the state level and the central level. Most of them have been replaced by GST, making the entire tax structure much simpler and there is no confusion and entanglement at the business end, as they have to comply with only one tax.

Remove Multiple Indirect Taxes is the 16th objective among the objectives of GST and also a very important one.

Increasingly Efficient Logistics

GST has helped remove inter-state tax barriers and improve logistics efficiency. Goods can now be transported efficiently without the hassle of multiple tax payments and clearances during transportation, reducing costs involved in transportation and delays.

Increasingly Efficient Logistics is the 17th objective among the objectives of GST and also a very important one.

Review Tax Revenue

GST will ensure periodic monitoring of collection and compliance levels, so as to provide a steady flow of revenue to the government. Using a data approach, it is possible to adjust tax rates and policies in a timely manner so as to maintain the budget stability of this state.

Review Tax Revenue is the 18th objective among the objectives of GST and also a very important one.

Uplifting GDP

GST contributes to the country’s economic growth and overall GDP, as it simplifies taxation and promotes the export of goods, thereby reducing the cost of production of goods. The ease of doing business in GST attracts more investment and entrepreneurial activity, making the economy healthier.

Uplifting GDP is the 19th objective among the objectives of GST and also a very important one.

Better Tax Management

A much more organized system of tax collection and management has been incorporated by GST. Since the taxation process is also digital, proper records can be maintained along with timely payment, so both businesses and the government can easily manage taxes.

Better Tax Management is the 20th objective among the objectives of GST and also a very important one.

Broadening the Tax Base

GST brings more businesses into the formal tax system because it makes taxation easier, and thus there is less chance of evading taxes. Increased revenue also leads to better public service and physical infrastructure development.

Broadening the Tax Base is the 21st objective among the objectives of GST and also a very important one.

Composition Scheme for Small Businesses

The idea behind the composition scheme is to relieve small businesses from the difficulties faced in GST compliance. To avoid the creation of cumbersome paperwork, this scheme allows small businesses to pay a fixed lower rate of tax on turnover. This reduces their compliance burden and tax liability, making it easier for them to operate under the GST framework.

Composition Scheme for Small Businesses is the 22nd objective among the objectives of GST and also a very important one.

Regulation of Unorganized Sector

GST will bring the unorganized sector under formal regulation by simplifying tax compliance and reducing the scope for tax evasion. Hence, there will be greater accountability, and it will encourage businesses to get registered and comply with tax laws.

Regulation of Unorganized Sector is the 23rd objective among the objectives of GST and also a very important one.

To Increase the Productivity

GST will improve productivity as it eliminates and reduces tax-related inefficiencies. With a uniform system of tax collection, business firms can use their resources better and produce more instead of tinkering with complex tax rules.

To Increase the Productivity is the 24th objective among the objectives of GST and also a very important one.

To Reduce the Prices

To reduce the tax burden on businesses, GST reduces it. This in turn forces business houses to reduce the prices of their products and services. Cascading taxes are eliminated with input tax credits so that manufacturers and suppliers can pass on the savings to consumers.

To Reduce the Prices is the 25th objective among the objectives of GST and also a very important one.

Dynamic Common Market

GST has created a vibrant common market under which all goods and services can move freely within states without any taxes. This in turn helps to promote trade and investment; hence, leads to development at the state and national level as well.

Dynamic Common Market is the 26th objective among the objectives of GST and also a very important one.

Simplification of Taxation

GST has replaced India’s complex multi-tax structure with a simpler and more transparent system. This has reduced confusion for businesses, reduced compliance costs, and even made it easier for everyone to understand their obligations in taxes.

Simplification of Taxation is the 27th objective among the objectives of GST and also a very important one.

Streamlined Online Procedures

The process is also online, which improves the speed and accuracy of filing returns, paying taxes, and issuing refunds. This reduces delays and errors and reduces the burden of administrative and bureaucratic systems on businesses.

Streamlined Online Procedures is the 28th objective among the objectives of GST and also a very important one.

A Uniform Tax System

GST is a uniform tax levied on goods and services across the country. It has eliminated the clutter of tax rates and different rules across states.

A Uniform Tax System is the 29th objective among the objectives of GST and also a very important one.

Enhanced Productivity of Logistics

The removal of checkpoints at inter-state check posts and streamlined tax processes at GST has made logistics much more efficient. This is because goods are moving faster which reduces the time and cost of transportation, and thus overall increases the overall productivity in the logistics sector.

Enhanced Productivity of Logistics is the 30th objective among the objectives of GST and also a very important one.

GST Rates on Goods and Services

With different tax rates on various categories of goods and services under GST, basic products will have the lowest tax rates and luxury products will have higher tax rates. Hence, this form will maintain the practice of fair taxation and also curb excessive consumption of every good and service.

GST Rates on Goods and Services is the 31st objective among the objectives of GST and also a very important one.

If you want to know about the objectives of GST explained by a person then you can click on the video given below:

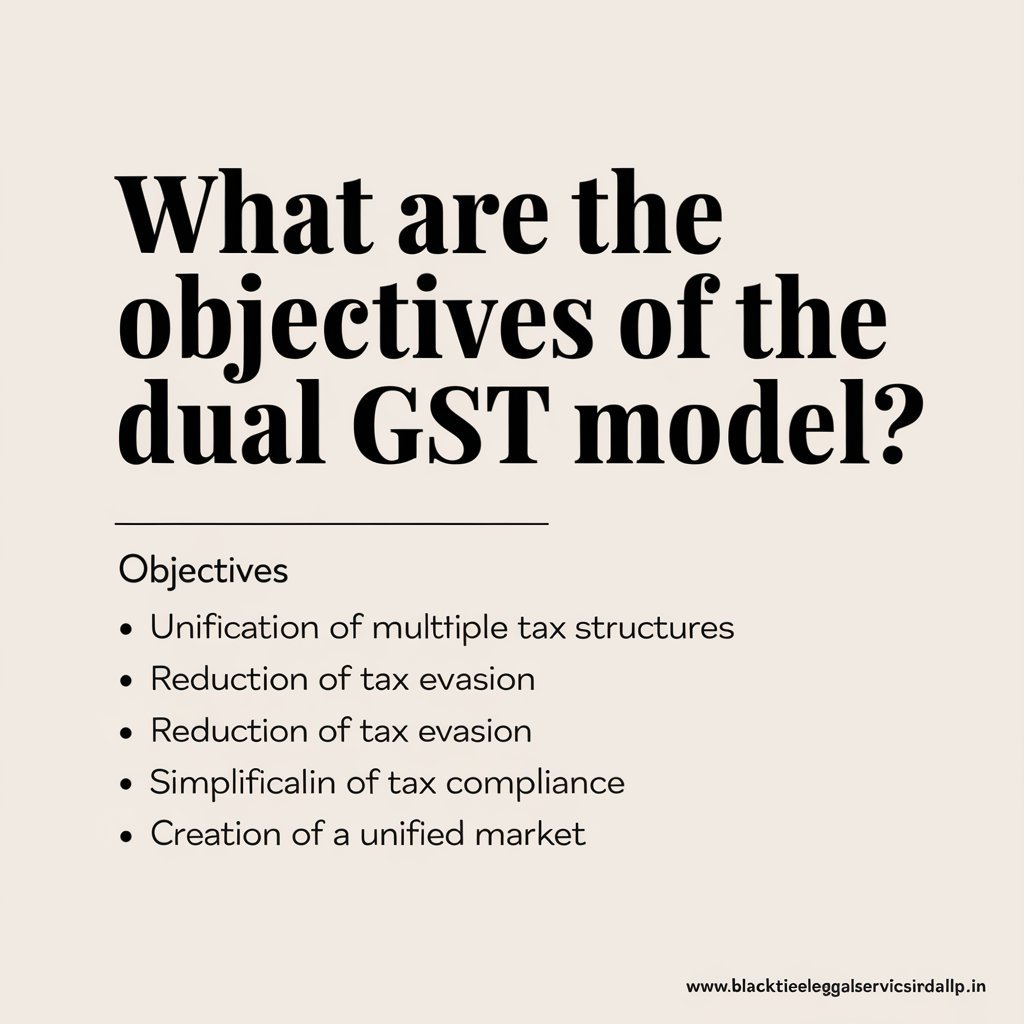

What are the Objectives of the Dual GST Model?

We have briefly summarized the Objectives of the Dual GST Model below:

- Federal Structure Compliance: The dual GST model is a model completely conforming to the federal structure of India. It allows both the central and state governments to collect taxes on goods and services.

- Equal Revenue Sharing: This ensures that the revenue sharing between the central and state governments is equal.

- Avoids Double Taxation: With both, especially the Central GST and State GST, the dual GST model ensures that there is no double taxation, and will promote ease of doing business.

- Tax Uniformity: It maintains the standardization of tax at all levels in the country while giving some operational freedom to the states.

What are the Main Features of GST?

If you want to understand the features and salient features of GST very well then you can click on here.

What are the Types of GST?

We have briefly summarized the Types of GST below:

- CGST (Central Goods and Services Tax): A duty levied by the central government on sales made within a state.

- SGST (State Goods and Services Tax): State governments collect tax on sales made within the state.

- IGST (Integrated Goods and Services Tax): This is levied on inter-state sales, which are collected by the central government and shared with the states.

- UTGST (Union Territory Goods and Services Tax): This applies to union territories where there is no legislation, a form of SGST.

If you want to know about the types of GST explained by a person then you can click on the video given below:

What are the Advantages of GST?

If you want to know about the advantages as well as disadvantages of GST then you can click on here.

In Conclusion

GST has brought a paradigm shift in India’s taxation landscape by eliminating the cascading effect of taxes, simplifying the tax structure, and complementing the ease of doing business with tax compliance. It supports the growth of the economy by establishing a unified national market, boosting exports and productivity. Cooperative federalism as well as effective tax management and broadening of the tax base are the aspects that GST hopes to take forward to create a competitive and vibrant economy for the future.

FAQs

Q1. What are the aims and objectives of the CGST act?

It aims to levy and collect tax on the inter-state supply of goods and services, ensuring uniformity in tax rates, thereby smoothening the process of tax collection and reducing complexities in compliance.

Q2. What is the objective of supply under GST?

Under the GST framework, taxable supply is defined as the purpose of supply that involves the transfer of goods or services, and this forms the basic basis for levying GST on transactions.

Q3. What are the objectives of GSTR 3B?

This would mean adding up the total GST liability of the taxpayer and making timely payments to avoid paying interest and penalties through regular monthly self-declared returns, GSTR-3B.

Q4. What is GSTR-2 in GST?

GSTR-1 will report outward supplies or sales while GSTR-2 will report inward supplies or purchases. Then there is GSTR-3B, which is another summary return to be submitted monthly for tax payment.

Q5. What are GSTR-1 2 and 3B?

GSTR-1 reports outward supplies or sales, GSTR-2 reports inward supplies or purchases and then comes GSTR-3B, which is the third- monthly summary return for tax payment.

Q6. How to calculate GST?

GST is figured out by multiplying the value of taxable goods or services on which duty is to be paid by the applicable GST rate, which can be 5%, 12%, 18%, or 28%, depending on the category.

Q7. What is a drawback in GST?

GST refund: This is the amount of duty paid at the time of import when those goods are re-exported. This gives relief to exporters.

Add a Comment