Tax planning is one of the subcategories of financial planning, which aims to reduce the total tax to be paid by a business, while at the same time staying legally compliant.

It refers to the process of minimizing the amount of tax to be paid by employing techniques, exclusions, reliefs, and others allowed in the tax laws.

However, tax planning, like any other planning, has its limitations. It is important that people and organizations fully understand these limitations to avoid such issues and be compliant with taxation laws.

This blog post looks at the various aspects of the top 14 limitations of tax planning and looks at how these affect the person discriminating in tax planning.

What is the Tax Planning?

Tax planning involves structuring affairs in the most advantageous tax-efficient manner in accordance with the law. It involves proactive techniques of budgeting, earning, spending, investing, and claiming in order to pay as little tax as legally possible.

Tax planning is the process of making appropriate adjustments in a person’s case so that he takes full advantage of all legal exemptions, deductions, credits, and any other type of concession allowed under the tax laws so that he can legally reduce his tax liability.

What are the Top 14 limitations of Tax Planning?

We have presented to you all the top 14 limitations of tax planning; a good amount of information has been provided below, which will help you in tax planning; you will get all the information that no one else has been able to provide you till now:

- Legal Risks and Changing Regulations

- Time and Resource Intensive

- potential Cash Flow Issues

- Dependency on External Factors

- Complexity of International Tax Planning

- Risk of Audit and Scrutiny

- Complex Tax Laws

- Limited Time and Resources

- Uncertainty in Future Tax Rates

- Short-Term Focus

- Risk of Tax Evasion

- Changes in Personal or Business Circumstances

- Potential Costs of Implementation

- Limited Awareness of Available Opportunities

Legal Risks and Changing Regulations

Legal Risks and Changing Regulations are some of the biggest problems of tax planning: this subject is characterized by constant changes in the law. It is therefore important to keep in mind that tax laws can vary greatly over time depending on the political or economic situation and certain administrative decisions. These changes can affect existing tax planning methods making them ineffective or irrelevant.

Legal Risks and Changing Regulations are the 1st limitation among the Top 14 limitations of tax planning and also a very important one.

Time and Resource Intensive

Time and resource intensive is generally expected that effective tax planning takes a lot of time as there is a wide range of tax planning tools and strategies available to taxpayers.

It is often the case that busy individuals and small business entities do not have the time to know all the laws governing their taxes or to plan adequately. Such a situation can lead to poor decision-making or no planning at all and rush through the decision-making process.

Time and Resource Intensive is the 2nd limitation among the Top 14 limitations of tax planning and also a very important one.

Potential Cash Flow Issues

Most tax planning strategies require the client to balance the amount of tax paid against the company’s needs which may sometimes be for a short-term cash flow. For example, income timing strategies such as observing increased income next year while expense timing includes assuming twice the expenses in the next year will lead to immediate cash flow constraints due to the achievement of strategic objectives.

Potential Cash Flow Issues is the 3rd limitation among the Top 14 limitations of tax planning and also a very important one.

Dependency on External Factors

Tax issues are subject to various external constraints such as those related to economic bullion, markets, and government policies. This means that changes in these factors can affect tax strategies and outcomes. For example, changes in interest rates or the occurrence of a recession can affect the efficiency of certain planning strategies.

Dependency on External Factors is the 4th limitation among the Top 14 limitations of tax planning and also a very important one.

Complexity of International Tax Planning

International tax planning is a challenge and comes with greater complexities for companies doing business in different countries. Laws of taxation and regulation vary from one jurisdiction to another, thus making the tax system somewhat inconsistent in terms of functionality and strategic planning.

A complex environment characterized by this commendable complexity requires a comprehensive knowledge of domestic and international taxation laws in an effort to succeed in this area.

Complexity of International Tax Planning is the 5th limitation among the Top 14 limitations of tax planning and also a very important one.

Risk of Audit and Scrutiny

Controversial planning strategies that are close to aggressive may be considered so by tax authorities, increasing the liability for an audit.

Nevertheless, since tax planning is legitimate, the legal difference between planning and evasion can sometimes be fragile and may involve the risk of legal consequences. A taxpayer must be prudent and most importantly, he must ensure that whatever strategy he is adopting is legal.

Risk of Audit and Scrutiny is the 6th limitation among the Top 14 limitations of tax planning and also a very important one.

Complex Tax Laws

The limitation of tax planning is that it is generally constrained by the legal issues of taxes. Due to frequent changes in tax laws around the world, tax matters are complex and can be difficult, especially for business entities and other players in the economy, to strike a balance between tax compliance and tax planning and strategies. It can be confusing and something may be missed and it may attract some other taxes or penalties for which the businessman may not be prepared.

Complex Tax Laws is the 7th limitation among the Top 14 limitations of tax planning and also a very important one.

Limited Time and Resources

Tax planning is a time-consuming process that requires a lot of effort. Small business entities and the general public may not have the knowledge or capital to hire professional tax advisors or conduct extensive analyses.

This simple logic leads them to adopt very basic tax planning strategies to minimize taxes that are not aimed at maximizing benefits and do not consider (or even prevent) potential allowances and deductions.

Limited Time and Resources is the 8th limitation among the Top 14 limitations of tax planning and also a very important one.

Uncertainty in Future Tax Rates

Tax planning also involves assumptions regarding potential taxes and the laws regulating this issue. However, all these assumptions can be unpredictable at some point.

Government policies, economic policies, and political changes can affect taxation policies in the future, making existing plans ineffective. This fact means that it is very difficult to formulate a long-term tax strategy and see it being valid even after some time.

Uncertainty in Future Tax Rates is the 9th limitation among the Top 14 limitations of tax planning and also a very important one.

Short-Term Focus

It is often seen that many people and companies think only about saving current taxes instead of thinking about their long-term wealth. Such myopia is seen when dealing with taxes, which means that some decisions will force the company to pay less tax in the current period while it will have to pay more in the subsequent period. For example, optimizing current tax shields can be costly for future cash flows or investment options.

Short-Term Focus is the 10th limitation among the Top 14 limitations of tax planning and also a very important one.

Risk of Tax Evasion

While tax planning is legal and recommended, it is close to illegal tax avoidance, if not even part of it. This means that legal fights and audit activities in today’s economy pose significant threats to various serious and aggressive tax avoidance methods that are commonly known in the law.

Few companies engage in such discretionary activities because, despite the short-term gains from effective tax planning, they suffer greater losses in terms of penalties and reputation.

Risk of Tax Evasion is the 11th limitation among the Top 14 limitations of tax planning and also a very important one.

Changes in Personal or Business Circumstances

Personal or business circumstances can change unexpectedly, which can lead to changes in the efficiency of tax planning. Changes in the life of an individual or organization can have a huge impact on its tax scenario such as marriage, divorce, job changes, or selling a business. A certain tax plan that may have worked well may change or bring less benefit, requiring constant review and revision.

Changes in Personal or Business Circumstances is the 12th limitation among the Top 14 limitations of tax planning and also a very important one.

Potential Costs of Implementation

The implementation of tax planning strategies involves cost factors, which reduce the benefits gained through tax planning. For instance, outsourcing employees to tax professionals or buying or subscribing to some of the best tax software also comes at a cost and can eat into the money saved.

Also, some of these tax strategies may require some modifications in the existing structures of finances and investment portfolios and may attract other additional expenses.

Potential Costs of Implementation are the 13th limitation among the Top 14 limitations of tax planning and also a very important one.

Limited Awareness of Available Opportunities

Some of these taxpayers may need to realize how many opportunities are available in terms of tax planning. Not knowing about tax credits, deductions, and incentives can result in investors suffering losses, resulting in wasted opportunities.

Those who follow the year under discussion and do not consider the issue of tax planning may end up paying more than the expected amount.

Limited Awareness of Available Opportunities are the 14th limitation among the Top 14 limitations of tax planning and also a very important one.

What is the Scope of Tax Planning?

The scope of tax planning covers a wide range of activities aimed at reducing tax liability through efficient financial management. It includes:

- Income management: Organizing income in such a way that maximum revenue is exempted and minimum deductions are made.

- Investment planning: Buying tax-saving products such as endowment policies, retirement pensions, and government-approved bonds.

- Expense management: Exempting deductions such as personal medical expenses, educational expenses, and home loan interest rates.

- Tax law optimization: Taking advantage of other provisions of the law to avoid paying taxes as much as legally possible, such as using accounting techniques to defer income and capital gains.

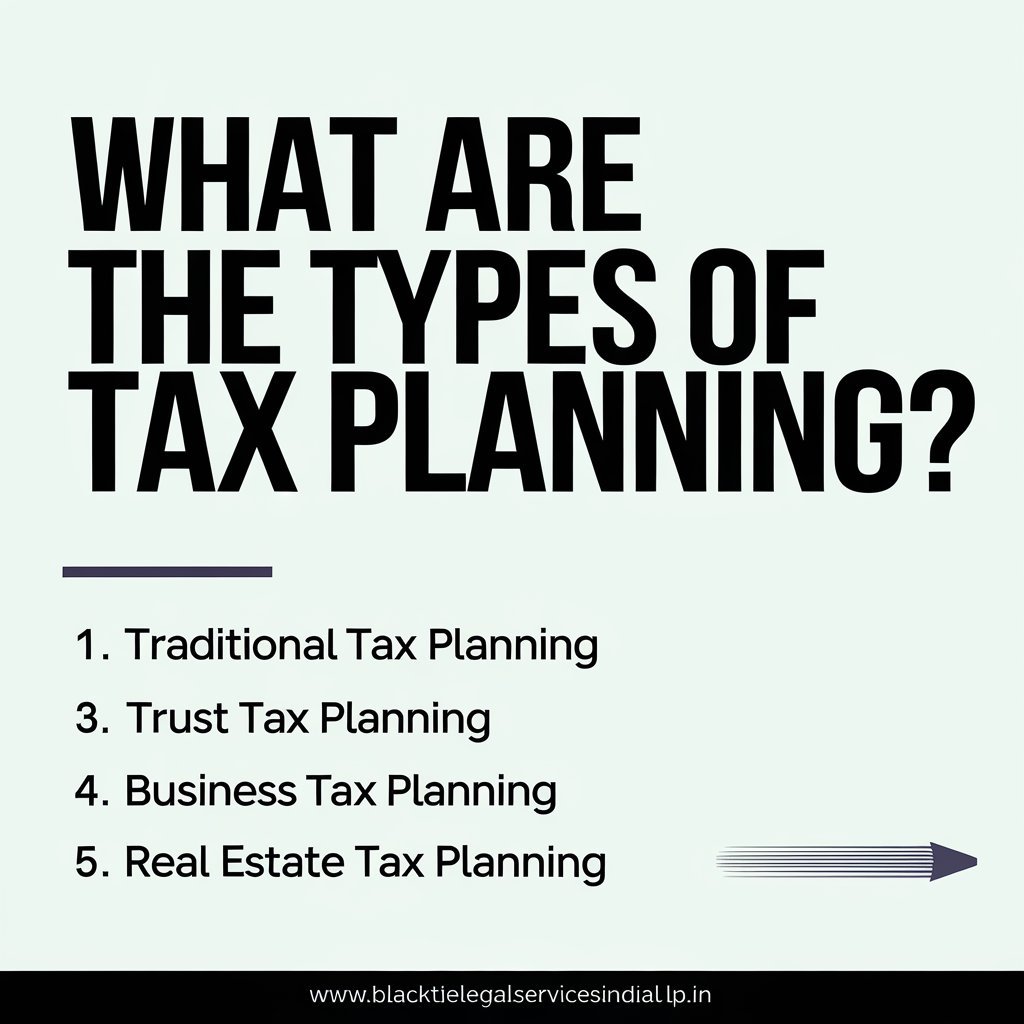

What are the Types of Tax Planning?

Here’s the complete guide to types of tax planning:

- Short-term tax planning: Based on activities undertaken in the last quarter of the financial year to directly reduce tax liabilities.

- Long-term tax planning: Refers to strategies developed to cover the entire year or even longer as they are in sync with other financial strategies.

- Permissive tax planning: Fully utilizes every legal allowance, deduction, and exemption available in the law to minimize taxes.

- Purposeful tax planning: Specific advice given for a particular goal or need, for example, in relation to retirement or an investment agenda.

If you want t know more about the types of tax planning the you can click on the below video

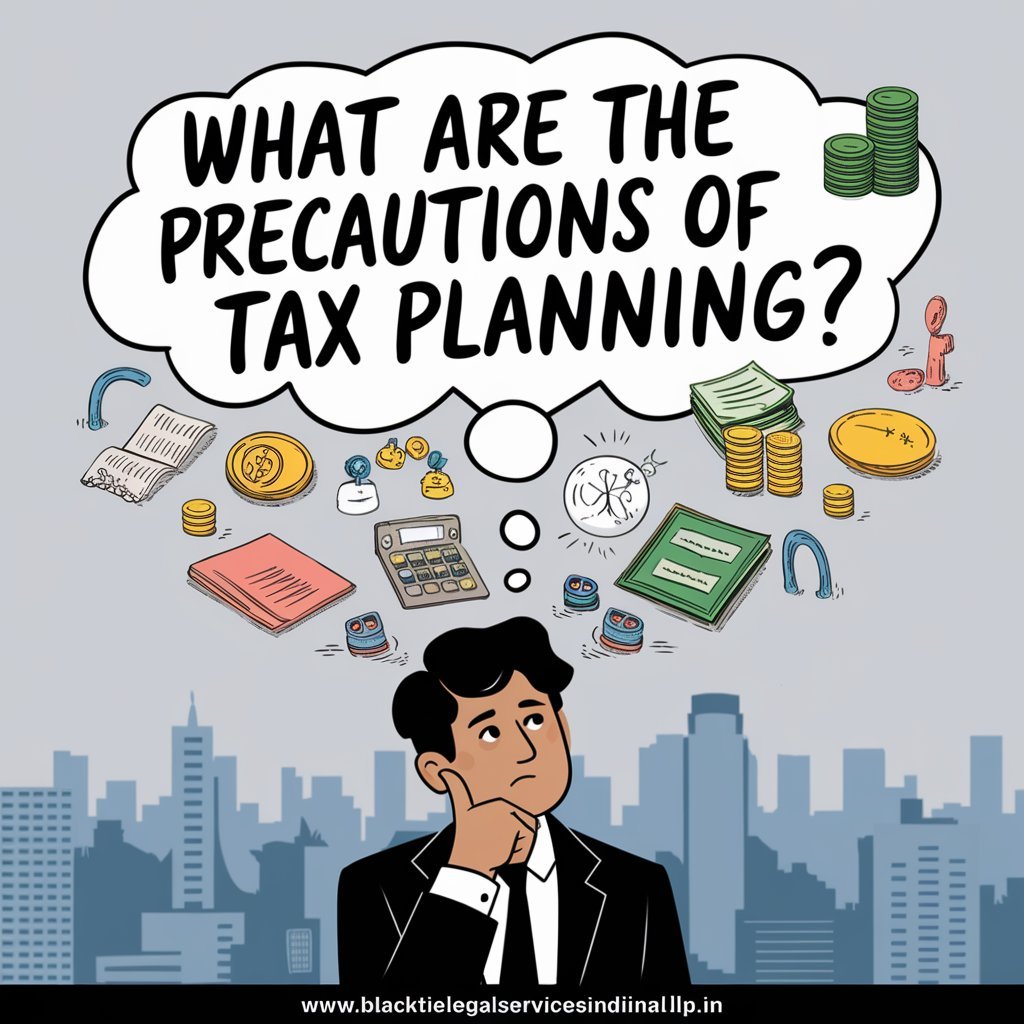

What are the Precautions of Tax Planning?

When engaging in tax planning, certain precautions should be taken:

- Comply with tax laws: Make sure they are valid, taking into account all legal tax-related complexities that may lead you to penalties or legal complications.

- Avoiding aggressive strategies: When it comes to tax planning, there is always a thin line between aggressive and evasive; the latter may attract auditors and the law.

- Balancing financial goals: The tax planning strategy should involve efforts to achieve the most financially appropriate goals and should not be at the expense of or sacrifice future benefits for current tax optimization.

- Consulting professionals: The complexity of tax laws is evident, so engaging a tax expert allows complying with the laws and utilizing the benefits in the best ways.

- Monitoring changes in tax laws: It is important to be flexible with tax planning for several reasons and the most important one is that tax laws keep changing frequently.

What are the Objectives of Tax Planning?

The primary objectives of tax planning include:

If you want to get the complete guide to the objectives of tax planning, then you can click here.

In Conclusion

While tax planning is an essential tool for managing tax liabilities, it is crucial to recognize its limitations. The complexities of tax laws, uncertainties about future regulations, and potential changes in personal or business circumstances can all impact the effectiveness of tax strategies.

By understanding the limitations of tax planning, individuals and companies can approach tax planning with realistic expectations and a more informed perspective, ensuring they make the most of available opportunities while remaining compliant with tax regulations.

FAQs

Q1. What are the limitations of the tax system?

The limitations of the tax system include complex regulations, frequent changes in tax laws, high compliance costs, unequal tax burdens, and the risk of tax evasion or avoidance.

Q2. What are the 5 D’s of tax planning?

The 5 D’s of tax planning are Deferral (postponing tax liability), Deduction (claiming allowable expenses), Division (splitting income), Discount (using lower tax rates), and Disguise (legally minimizing taxable income).

Q3. What are the principles of tax planning?

The key principles of tax planning are legality (following the law), financial efficiency, future foresight, alignment with personal or business goals, and flexibility to adapt to changes in tax laws.

Q4. What is a tax planning tool?

A tax planning tool refers to methods, strategies, or software used to calculate, reduce, or optimize tax liabilities, such as tax-saving investments, deductions, and credits.

Q5. What is the need for tax planning and what are its limitations?

Tax planning is needed to minimize tax liabilities, ensure financial efficiency, and comply with legal obligations. However, its limitations include legal risks, changing tax laws, and time-consuming efforts.

Add a Comment