Fringe Benefit Tax (FBT) in India was introduced through the Finance Act 2005. This tax was one of the milestones in the Indian tax system and was levied on ‘perquisites’ issued to employees by their employers, a very significant part of the employees’ remuneration, which are usually not included in the employees’ taxable income.

Fringe Benefit Tax (FBT) was used by the government in such a way as to tax such benefits, thereby expanding the tax base.

Though Fringe Benefit Tax (FBT) existed later till 2009, the establishment of fringe benefit tax (FBT), its implementation and its removal reflect its impact on employers and employees on non-cash benefits and incentives.

Through this blog post, we would like to let you all know about the overall origin, implications and eventual abolition of Fringe Benefit Tax in India along with its deep impact on businesses and employees.

Understanding Fringe Benefits

“ We would like to tell you all that before knowing about Fringe Benefit Tax, it is more important to understand the Fringe Benefits in detail so that you do not have to face any problem in Fringe Benefit Tax in future.”

What are the Fringe Benefits?

Fringe benefits are another type of remuneration provided to employees other than cash salaries. Such benefits may include a range of privileges, including medical care, automobiles, holidays, insurance, retirement and other financial rewards, as well as other privileges such as parking, meals, exercise facilities and stock options.

Perks are often given to employees to gain and retain employee loyalty and to supplement the employee’s income or provide him with some kind of psychological security.

However, in some countries, these benefits may be taxed beyond what is allowed under the country’s taxation laws.

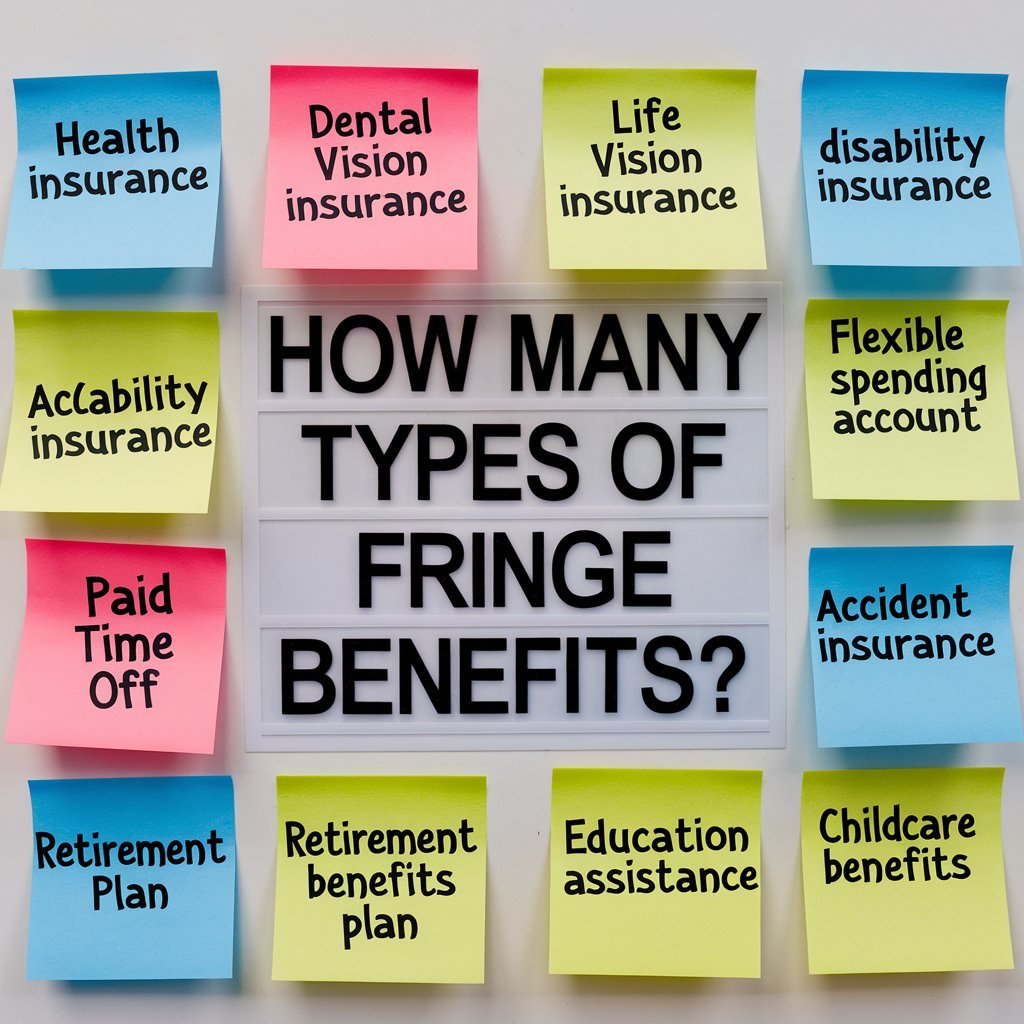

How Many Types of Fringe Benefits?

There are many different types of fringe benefits which are very important to know about, but we have discussed some of the main types in detail below:

Health and Wellness Benefits

- Health Insurance: All employee medical, dental and vision care needs are fully met.

- Gym Memberships: The opportunity to attend fitness clubs or use organized health promotion programs

- Mental Health Support: Counseling or anxiety reduction programs.

Financial Benefits

- Pension Plans: Pension benefits such as 401(k) in the case of the USA or EPF in the case of India.

- Bonuses and Stock Options: Bonuses in the form of more cash in addition to other incentives such as share options.

- Life Insurance: A benefit under which coverage is extended to an employee’s dependents in the event of his or her death.

Work-Life Balance

- Paid Time Off (PTO): Paid holidays, medical leaves, and other privilege.

- Flexible Working Hours: Things like remote work, compressed workweek, or flex.

- Parental Leave: Paid vacations and medical leave or childbirth and adoption; vacation for new parents.

Education and Training

- Tuition Reimbursement: Tuition fees for additional education and certification programs.

- Professional Development: A training that is financed by the employer, for example, through carrying out a workshop, seminar or even a course.

Transport and Travel

- Company Car: A car given to be used privately and also for official purposes.

- Travel Allowances: Expenses incurred in the course of business trips or where the company gains some advantage.

- Commuter Benefits: Subsidies for use of public transport or for car parking.

Miscellaneous Perks

- Meals and Entertainment: Meals, lunch, or dinner without charge or at a minimal cost, business trips, or tickets to predetermined events.

- Housing Allowance: Subsidization of living accommodations, especially for personnel of international organizations and companies.

- Childcare Services: Child care centres at the workplace or Child care allowance.

What is Taxation of Fringe Benefits?

In many countries around the world, certain benefits are considered taxable income. The rules are complex and depend on the jurisdiction, but in the most common case, the value of such benefits must be considered part of the employee’s compensation and may be taxed through payroll taxes.

Employers also have to be able to pay for Fringe Benefit Tax (FBT), which a tax imposed on employers in respect of certain benefits given to the employees.

Why do Employers Offer Fringe Benefits?

- Attracting Talent: Fringe benefits can help attract employees because they are tangible when used in the offer of a job.

- Employee Retention: High benefits are generally associated with a high level of job satisfaction and low turnover.

- Improving Productivity: Measures such as health promotion programs can bring mature and enhanced employees.

- Tax Advantages: There are periods and instances where it even is most advantageous to give benefits instead of increasing the amount of pay lets say.

Examples by Region

- United States: Such are the recognizable advantages, which may comprise medical insurance, a 401(k) plan, paid days off.

- India: Some of the more common are Provident Fund (PF), Employees State Insurance (EPF), and Gratuity.

- Europe: Paid holidays, paid medical and dental, and employee child care are usual benefits offered.

Understanding Fringe Benefit Tax

We have discussed fringe benefits in detail above, so now we will understand about fringe benefit tax.

What is the Fringe Benefit Tax?

Fringe Benefit Tax was a tax imposed by our Government of India on all kinds of fringe benefits provided by employers to their employees over and above the regular salary.

Although, the fringe benefit tax was not imposed in India for long, yet its introduction was a significant development in the Indian tax law with the main objectives being to expand the tax base and curb tax evasion.

What is The Rationale Behind Fringe Benefit Tax?

Non-cash benefits given by employers to employees, before the advent of Fringe Benefit Tax (FBT), were not considered taxable. This led to a system whereby all firms were able to provide considerable non-cash benefits to their employees that would not affect their taxable income.

Such expenses included company cars, entertainment costs, employee stock options, etc. and were often of very large value.

The Indian government realized that this was one of the loopholes that needed to be closed and hence introduced FBT.

The FBT scheme was explicitly designed by the Indian government to ensure that all employment incentives are taxable, whether in the form of money or not.

This was in line with global practices where such taxes were prevalent in other countries to ensure that allowances and other preferences given to workers are adequately taxable.

What are the Fringe Benefit Tax Exemptions?

In the previous system, specific requirements had to be met to make an employee exempt. The conditions entitling an employee to a prescribed amount of fringe benefits included period of employment, maximum limit of remuneration salary and the characteristics of the fringe benefit tax exemptions provided by the employer.

Here were the exemptions available before the Fringe Benefit Tax was abolished:

– Salary Threshold: The tax statute also excluded wages below ₹ 15,000 per month from FBT, and the employees receiving such wages were thus not subject to this taxation.

– Tenure with the Organization: In the case of FBT, all organizational expenses prohibitive to its fairness were discretionary, while additional years of service with an organization meant zero FBT for employees who had more than five years of service with an organization.

– Resignation Before Five Years: Those staff members who resigned with less than five years of contributory service in their former employers are charged FBT.

– Transfer to Another City: All transferred employees were also free from FBT provided that the transfer was from one city to another within the same organization.

How is Fringe Benefit Tax (FBT) Calculated?

FBT was levied on the value of fringe benefits provided by employers to employees. Like most taxes, the tax was calculated based on the cost incurred by the employer for these benefits.

The value of fringe benefits was estimated by factoring in the total expenditure incurred by the employer in respect of specific specified cost categories.

Categories of Expenditures

Under the Finance Act 2005 of India, various categories of expenditure were well specified which were completely subject to FBT. Out of which, we have mentioned some of the major categories in a proper manner.

- Entertainment Expenses: Expense incurred on general entertainments was given consideration for FBT purpose. A particular proportion of such costs was considered to be the value of fringe benefits.

- Hospitality: The area of expenditure which was liable for FBT was spending on hospitality, which covered food and beverages to be made available to employees.

- Employee Welfare: Any expenditure incurred on the welfare of employees, such as recreational facilities or health clubs, is considered for FBT.

- Conveyance: Providing transport facilities to employees also comes under FBT and expenditure incurred in this regard is also taxable.

- Sales Promotion and Publicity: This also includes advertising and sales promotion expenses, which potentially apply to FBT, as FBT was often used as a way of indirectly providing remuneration to employees.

What is the Fringe Benefit Tax Rate?

The Fringe benefit tax rates used to vary across India depending on the expenditure of all expenditures.

The Finance Act 2005 prescribed specific percentages for each category, which were then applied to the aggregate expenditure to determine the overall value of fringe benefits.

The employer was required to pay tax at a flat rate of 30% on this value plus any applicable surcharge and cess.

What is the Abolition of Fringe Benefit Tax?

The criticism and challenges related to FBT forced the Indian government to abolish it. The Finance Bill 2009 introduced by the then Finance Minister Shri Pranab Mukherjee abolished FBT from 1 April 2009.

The reduction in FBT was welcomed especially by the corporate sector which had been agitating for the abolition of FBT.

Reasons of Abolition

The Main reasons behind the abolition of fringe benefit tax are given below:

- Administrative complexity: The government recognized that FBT was a massive headache for businesses, especially SMEs, and involved a lot of bureaucratic processes.

- Negative impact on employee benefits: The cut in the employee privileges to cater for the imposition of FBT went in veryary with the government’s aim of improving on the welfare of the employees.

- Simplification of the tax system: FBT was eradicated as part of a package of measures to improve the efficiency of the taxation system that involves lowering of current compliance cost of taxpayers.

Impact of Abolition

The abolition of FBT brought a lot of changes to the corporate world and employees. For a while, FBT eliminated the need for employers to pay tax on fringe benefits offered to employees.

This resulted in an increase in the provision of company fringe benefits as organizations were now willing to offer incentives to their employees without the burden of additional taxes.

Is fringe Benefit Tax Direct or Indirect?

Fringe benefit tax is an indirect tax levied on employers for providing allowances to their employees over and above their regular salaries.

Hence, it also falls under the category of a direct tax, as the burden of the tax is ultimately passed on to all employees through lower wages or higher prices for goods and services.

In Conclusion

Fringe Benefit Tax was one of the most measured aspects in the taxation history of India. Originally billed as a practical tool for providing for transparency and fairness in the taxation of employee benefits it elicited much controversy and problems that would lead to its repeal.

From the case of FBT, one can understand better the processes of the formation of the tax policy, as well as the measures that should be initially taken to minimize confusion and to enhance general comprehensibility of the legislation in the sphere of taxation.

FAQs

Q1. What is the FBT exemption limit?

A1. FBT was abolished in India in 2009. This means that the Fringe Benefit Tax now has no exemption limit as it did in previous years. So employers may offer some extra forms of remuneration to the employees, such as fringe benefits, with no extra tax charges.

Q2. What types of benefits were subject to FBT?

A2. The ATO-prescribed FBT-permissible benefits were, but were not confined to, cars provided for employees’ private use, fully and partly expensed accommodation, share incentives, meals, entertainment and amusement, gifts, and associate memberships.

Q3. Who was responsible for paying FBT?

A3: The FBT was charged to employers and not employees. The employers were liable to pay FBT on the fringe benefits which they offered to their employees.

Q4. How were employee benefits taxed after the abolition of FBT?

A4: Subsequent to the elimination of FBT, the treatment of employee benefits resumed the system of taxing the perquisites of the employees on a perquisite basis as part of the taxable income of the employee.

Q5. What was the compliance requirement for companies under FBT?

A5: The law meant that companies needed to provide records of those expenses chargeable to FBT, file FBT returns and pay tax on the value of the fringe benefits given in the financial year.

Q6. Were there any legal challenges to FBT?

A6. Yes, FBT encountered some legal problems from the businesses and the industry which considered the tax as unfair and cumbersome.

Add a Comment